Amidst rising inflation, food and energy supply disruption, falling tech stock valuations, and global conflicts, this is a synthesis of the key ideas shaping our view of the near term impact on the early-stage venture ecosystem, and founder resilience.

Key Takeaways

- Listed tech valuations are falling, with a trickle-down effect on the fundraising lifecycle for startups at all stages;

- Expect less direct investment activity from (some) business angels, corporates and family offices for which ventures is not a core allocation;

- VCs have a lot of dry-powder, and are eager to capitalise on outlier performance empowered by new market shifts, but expect investments to be more selective and concentrated;

- Every company is unique, and its fundamentals uniquely affected by a downturn — the market correction and changing environment will lead to great opportunities for some, yet difficult challenges for others;

- There will be a premium for startups that are lean, efficient and demonstrating signs of profitability (vs. growth at all cost), whilst adding real, sustainable value to their customers and/or users;

- The earlier stages of venture valuations are relatively insulated, with investment horizons of 5–10 years;

- Layoffs and inflation will affect tech employees and their livelihoods, hopefully not for an extended period of time;

- The cost of capital has increased across the board: valuations should come back to earth and round sizes become smaller — although with varying effects on the most competitive vs. average deals.

What to expect from tech startup valuations and the fundraising landscape in 2022

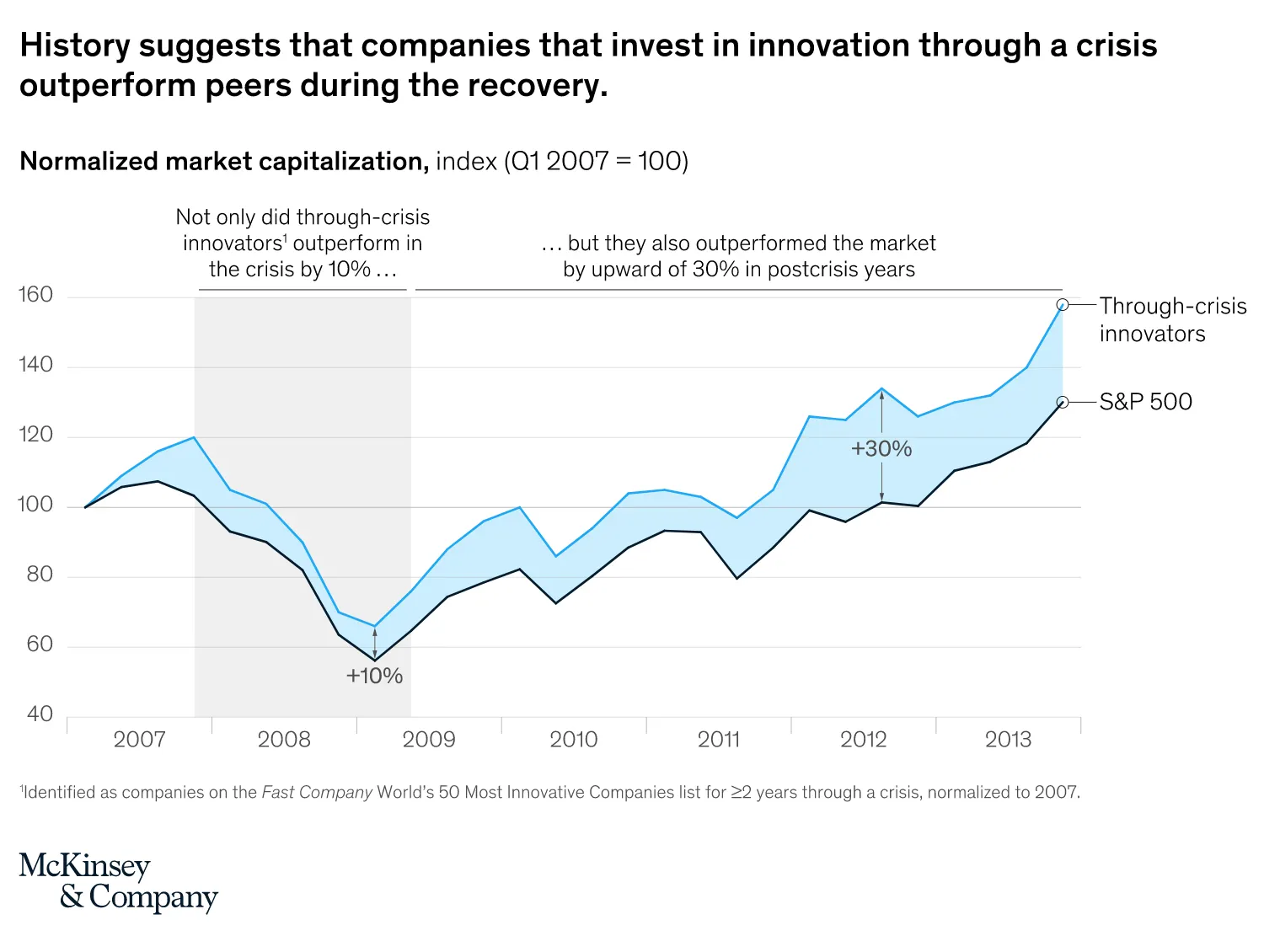

Kyle O’Brien, operating partner at VC firm Revaia, makes a compelling case for Maintaining Optimism in a Downturn. Looking at the underlying fundamentals for crypto — still a nascent asset class representative of the newest initiatives within tech— there is some hope that the correction we are seeing unfold will be beneficial in the long run: learning from the lessons of some dire failures (Celsius being the most recent to try and weather the storm), only the top performing crypto related projects will emerge as viable. At the same time, multiples for the top 10 Software companies were cut by more than 50% (average EV/NTM Rev multiple dopping from 59x to 24x from November 21 to April 22), but again, despite the belt-tightening and short term losses, past experiences would indicate that an economic downturn is possibly the best time to build and leapfrog the competition. Investing in innovation during a crisis has proven to lead to a 10% outperformance of the innovators compared to the S&P 500 in the midst of the downturn, and up to 30% outperformance in the post-crisis era. As an industry, VC is seeking to foster outlier performance spurred on by sustainable innovation and dynamic shifts in market conditions over long term horizons.

As an industry, VC is seeking to foster outlier performance spurred on by sustainable innovation and dynamic shifts in market conditions over long term horizons.

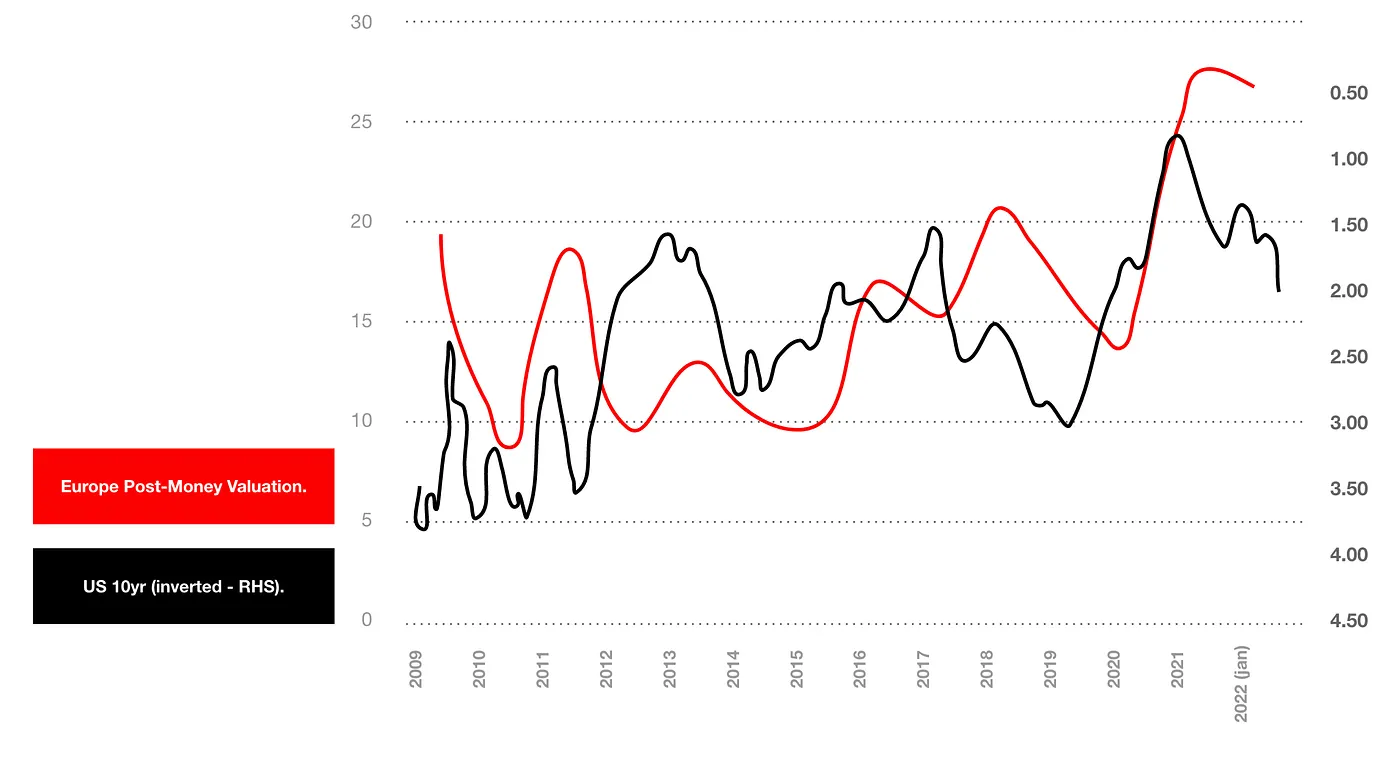

Cherry Ventures have shared their letter to their portfolio companies, summarising a few key insights into the fundraising landscape. NASDAQ is now down 29% YTD, SPACs and IPOs were down near 50% quarter-on-quarter, while stock markets with elevated volatility levels are indicative of worse IPO performance. The impact should trickle down to affect startups at all stages, leading to smaller rounds sizes and lower valuations on average. While European VC deployment and activity remained mostly intact during Q1 of 2022, it is likely to mimic the trajectory of the US ecosystem for which investments were down 23% in Q1 2022. With a certain time lag, shifts in the yield curve tend to positively correlate with changes in VC post-money valuations, suggesting valuations will continue to fall and cost of capital increase.

Data from PitchBook and CB Insights showed that VC activity globally had remained generally unaffected by the pressures that market turmoil had put on larger tech companies in the first quarter of the year. While the data is still preliminary, it seems that the private markets are catching up with the public market trends: global funding for the second quarter is projected to decrease by 19% quarter-over-quarter, deals are on track for a 22% drop from Q1’22, global M&A activity in Q2’22 is projected to drop by 22%, mega-rounds (deals worth $100M+) are projected to drop 18% QoQ and quarterly unicorn births are on track to fall below 100 for the first time since 2020. These shifts will affect the investment landscape and realised returns increasingly, the larger the companies and the closer they are to an IPO, liquidity or fundraising event. Again while these averages are telling, the specifics of each firm, their customers and their relative standing within the competitive landscape deserve to be taken into account in order to properly assess valuations and investment opportunities that might arise from such a downturn.

What does all of this mean for founders?

There has been some great advice shared by some very experienced people, entrepreneurs and investors, a few of which I would like to refer to here:

- Index Ventures’ advice on How Startups Should Handle a Downturn — every situation and startup is different and uniquely affected by a downturn;

- Sequoia’s workshop slides on how to adapt your business to endure during a crisis — the most adaptive companies will survive and thrive;

- YC’s words of caution to founders — the overall fundraising landscape is changing to become more demanding. Founders should take a moment to acknowledge that, and make sure their business is lean and resilient;

- David Sacks’ (Craft Ventures) very helpful tool— the Burn Multiple — for startups to assess and think about their capital efficiency.

I encourage both founders and tech investors to read thoroughly.

In short, the fundraising landscape for early-stage ventures will become more stringent and demanding: fewer investors (and less capital) will lead to fewer investments being made at an increased cost per capital. In practice it means founders will likely have to choose between smaller round sizes at lower valuations or, keeping round sizes intact, contend with being more diluted (I recommend the former when possible). There will be a premium for startups able to demonstrate that they are extremely lean and efficient at leveraging their resources with a clear path towards hard figures (revenues, margins and profitability). In the context of an early-stage company, founders have the relative luxury of time and are building a business over many years. The current sentiment and corrections will come to pass and new ups, downs, market swings and opportunities will arise along the journey.

In practice it means founders will likely have to choose between smaller round sizes at lower valuations or, keeping round sizes intact, contend with being more diluted (I recommend the former when possible).

Once we are able to acknowledge the current state of the financing landscape, I believe there are no silver bullets or one-size-fits all approaches to navigating the downturn. Each founder will face unique, at times very difficult, challenges as well as opportunities, but the main message remains that fundamentals now trump growth at any cost. Founders who focus on adding real, sustainable, value will thrive by addressing pressing real world issues (social, climate and productivity/market inefficiencies in particular), making sure their customers unconditionally love their product and are willing to pay for it, not being wasteful with their resources, taking good care of people who work for them and being mindful of the long path ahead.